News and Analysis of Foundation Investment Performance

Fourth Quarter Investment Performance

By

Solid Fourth Quarter Returns Across the Board

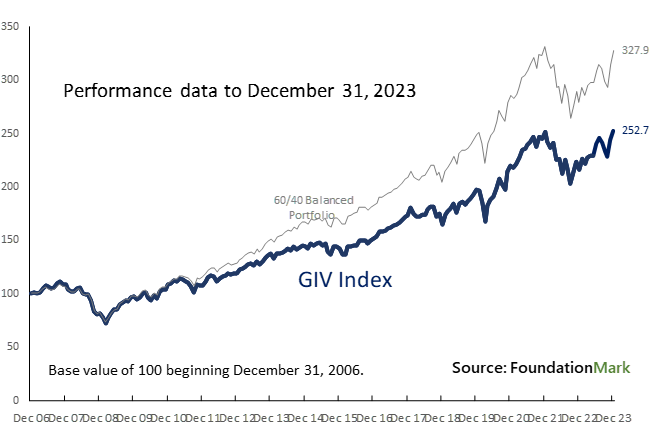

The Grantmaker Investment Value Index (“GIV”) rose 8.5% in the fourth quarter bringing full year 2023 performance to a 17.3%, the second best year in the past decade. Foundation investment performance annualized at 6.3% per year for the ten years ended December, 2023, modestly ahead of the required 5% payout ratio, but still well below the 60/40 mix (the traditional mix of 60% S&P 500 and 40% Bloomberg Aggregate Index) performance of 8.1%. While the difference of 1.8% might seem modest, over 10 years it accrues to about 20% of cumulative underperformance.

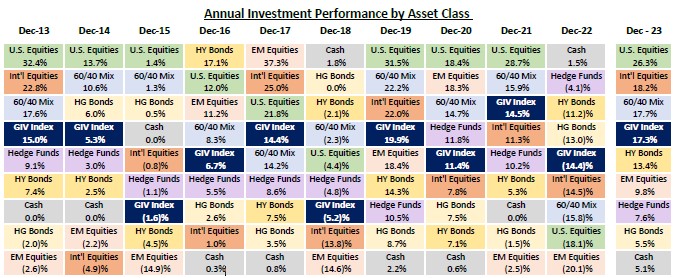

U.S. equity markets had a strong fourth the quarter, up 11.7% to close the year up 26.3%. International developed markets performed well, posting gains of 10.4% for the quarter and 18.2% for the year. Emerging markets trailed the U.S. for the ninth year out of ten, with gains of 7.9% for the quarter and 9.8% for the year.

U.S. high grade bonds’ 6.8% return in the fourth quarter brought full year performance back to positive territory, finishing the year up 5.5%. High yield bonds had a solid quarter, returning 7.2% and 13.4% for the year.

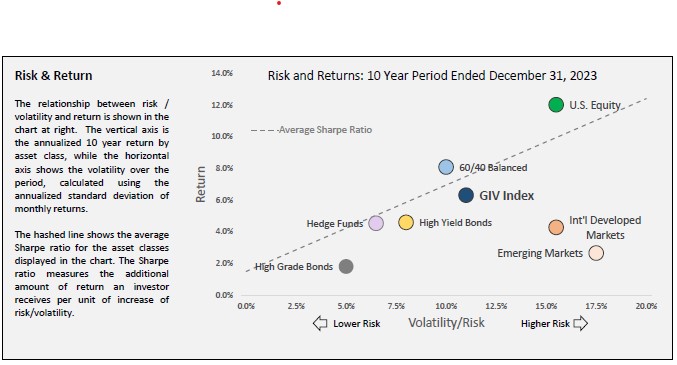

Risk and Return

The chart below shows the relationship between risk and return. In the chart risk is defined as volatility (shown on the x-axis) and return is plotted on the y-axis. Asset classes out to the right (International and Emerging Markets) are more volatile than those closer to the axis (High Grade Bonds). As one can see, over the 10-year period, U.S. Equities were the strongest performer, up 12.0% (y-axis). The dotted line shows an approximation of the average Sharpe ratio which is a measure of risk weighted return. Asset classes above the line delivered better risk/return than those below. U.S. Equity was the lone outlier over the period (which also drove the 60/40), with Hedge Funds approaching the average line.

As one can see Emerging markets were a poor asset allocation choice for the decade, with annualized returns of just 2.7% and volatility greater than U.S. Equity markets.

Over the 10-year period to December 2023, U.S. equities delivered close to three times the return of international stocks with a similar risk profile.

The FoundationMark GIV Index is calculated using FoundationMark return estimates up to and including December 2022 thereafter monthly returns are estimated based on reported asset allocations and market returns. The GIV Index serves as a proxy for foundation performance. Actual performance may differ materially. The GIV Index is updated on a continuing basis and all data is subject to revision.

The 60/40 Balanced Portfolio represents the traditional institutional allocation to equities and fixed income with weightings of 60% in the S&P 500 and 40% in the Bloomberg U.S. Aggregate Index, rebalanced monthly.