News and Analysis of Foundation Investment Performance

Disbursements Forecast Update: June 2024

By

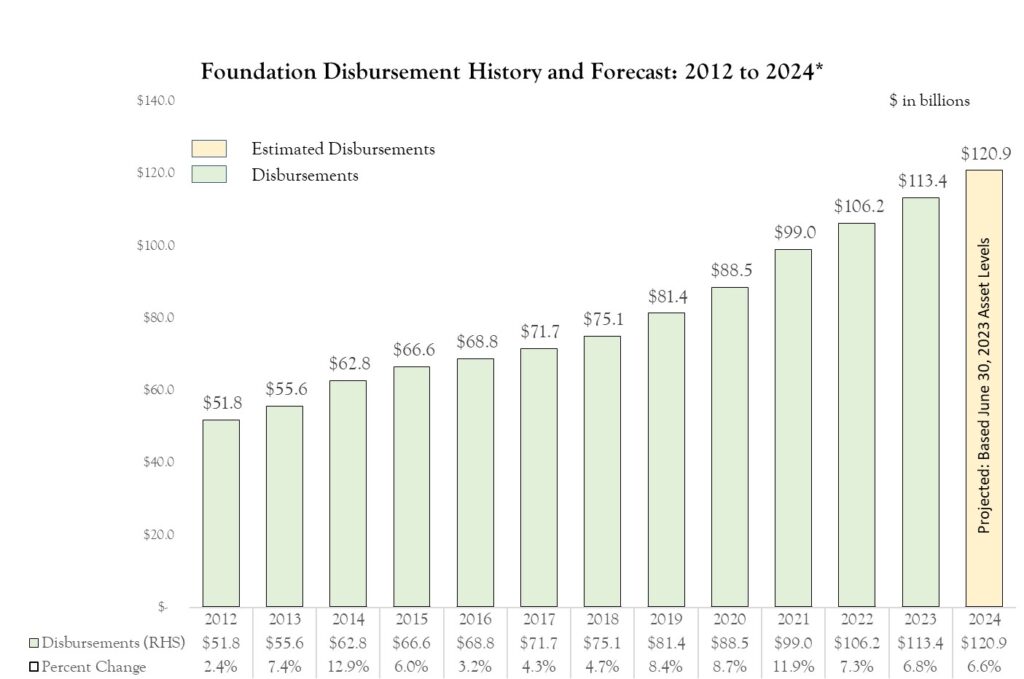

Disbursements Projected to Increase 6.6% in 2024

Disbursement projections are a function of two variables; 1) asset level, and 2) payout ratio. Estimated June 2024 foundation assets reached a record $1.6 trillion, up nearly $280 billion from 2022.

Based on the two important caveats (see box) regarding asset levels and payout ratios that we highlight, we project foundation disbursements to rise 6.6% to $121 billion in 2024 versus $113 billion in 2023.

Two Important Caveats

Disbursement amounts are based on two variables, 1) Asset Value, and 2) Payout Ratio.

Asset Value: The giving assumption is based on June 2024 estimated foundation asset levels of $1.6 trillion.

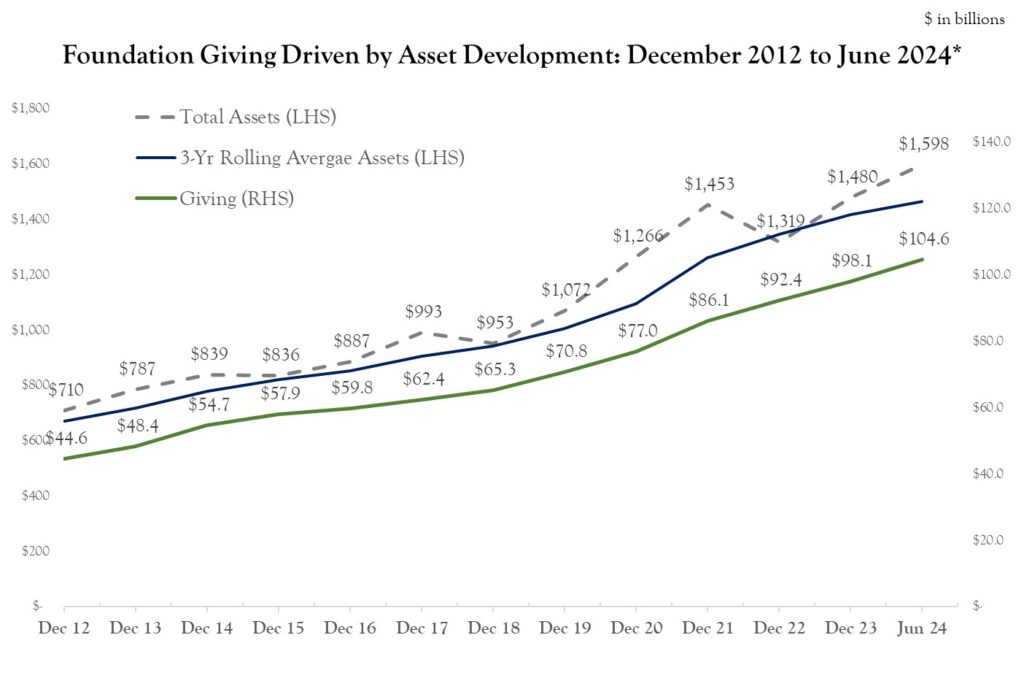

Payout Ratio: Historically, the foundation payout ratio has been about 8% of the three year rolling average asset levels. (see graph below)

*Annual giving levels shown above reflects total grants, gifts, and operating expenses as reported by private foundation in their 990-PF filings. There is a time lag between foundations year-end and when their tax filings are released to the public. Data for 2023 is preliminary and data for 2024 is forecasted based on the assumptions detailed below.

Historical Asset Level and Payout Relationship

As you can see in the graph below, there is a very high correlation between asset levels (light blue line) and disbursement levels (green line). Furthermore, one can see that while both assets and disbursements have shown significant growth over the period, asset levels tend to fluctuate more than disbursement levels, which is understandable as asset levels are subject to financial market moves. One reason for the lower volatility of disbursement levels is that many large foundations (which also represent a major proportion of charitable support) use a three year rolling average of assets when budgeting their grantmaking programs. The dotted line shows the three year average asset levels. The correlation coefficient between the three year average and disbursements is over 99%.

Disbursements versus Giving

The term “giving” is never mentioned in the IRS Form 990 PF, which is the source data for all our financial reporting, estimates, and projections. Instead, the tax form requires that foundations report their “Total Operating and Administrative Expenses” and “Total Grants, and Gifts Paid” – the total of these two lines is “Total Disbursements”. In another place on the tax form, foundations must report “Disbursements for Charitable Purposes”, which one might refer to as “giving” since it represents the amount, either in grants or expenses, that count toward the 5% payout requirement.

We refer to disbursements in this note as it provided the most comprehensive picture of foundation outlays. Historically, total “Disbursements for Charitable Purposes” is about 90% of “Total Disbursements”.

While we won’t know for sure the complete level of 2023 foundation disbursements until after every foundation has closed its books for the year, filed their 990-PF forms, and the IRS releases the data (though we have heard from about half of them), we believe that operating charities received about 6.8% in additional giving from foundations (see caveats above) versus 2022.

As we have noted, the relationship between giving and asset levels is very highly correlated. Hence, projecting giving implies projecting asset levels. And, asset levels can be very volatile. Nonetheless, we project giving levels based on current asset levels to help grant seekers better understand the financial position that foundations are currently in. As noted above, the financial position for foundations as of June 2024 is better than the start of the year and better than it was one year ago, and we expect 2024 giving to be just under $105 billion in 2024.