News and Analysis of Foundation Investment Performance

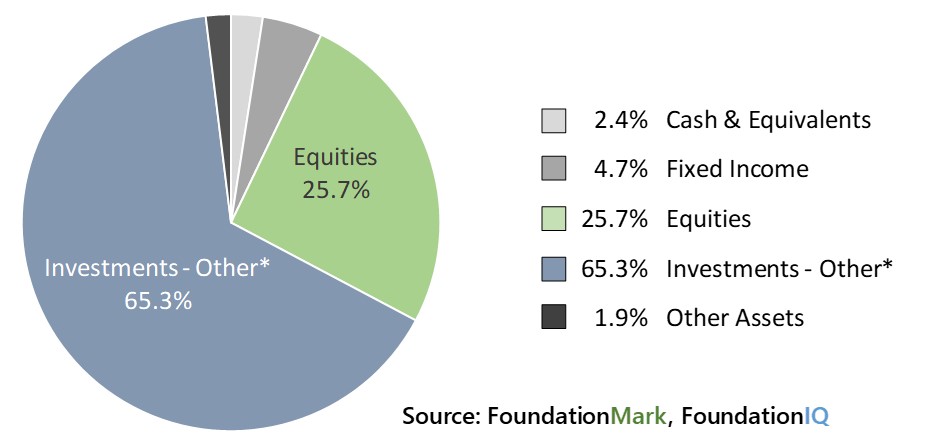

FoundationMark 15 Asset Allocation

By

The FoundationMark 15

The FoundationMark 15 (“FM 15”) is a selection of 15 of the largest and best-known private foundations in the United States. Most private foundations, like those comprising the FM 15, rely on their investment returns as an important, and, often, their only, source of income to support their philanthropic goals. To view the performances and full financial statements of these foundations, please visit FoundationMark 15.

Asset Allocation* of The FoundationMark 15

Investments – Other is a distinct line in the 990 – PF tax form that private foundations must file annually. The underlying investments represented in this line can include hedge funds, private equity holdings, privately held stock, venture capital, and more. Therefore, to ensure transparency and consistency, we include it as a distinct asset class just as the foundations reported it.

*A foundation may select any month end to be its fiscal year. Most members of the FM 15 use the calendar year, so the asset allocation reflected in the chart and referenced throughout is article is typically for the period ending December 31, 2017.

Not Many are "Average"

The FM 15’s allocation chart shown above might lead one to conclude that foundations have widely adopted the “endowment model”, which favors high allocations to private equity and hedge funds (typically included in Investments – Other). However, this is only partly true. Looked at individually, the FM 15’s asset allocations reveal many different approaches.

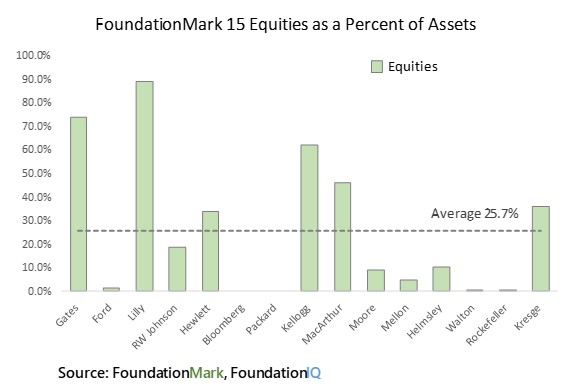

Equity Allocation

As you can see from the chart below, some foundations, notably Gates and Lilly, had very high allocations to Equities as of December, 2017, whereas others reported little to none. The 25.7% average allocation to Equities may be misleading as it bears noting that some foundations “kitchen sink” their allocation disclosures into Investments – Other (that is, throw everything but the kitchen sink into this category) by wrapping them in an investment vehicle or other means of obfuscation.

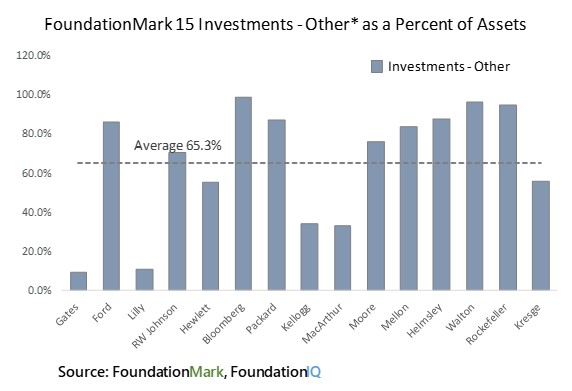

Investments - Other Allocation

As noted above, the Investment – Other line on the foundation’s balance sheet typically includes such alternative assets as hedge funds and private equity. Ford is a good example of this, as the additional information it provided on its 2017 holdings revealed over 80% in alternative strategies including private equity, venture capital, and other alternative investment strategies.

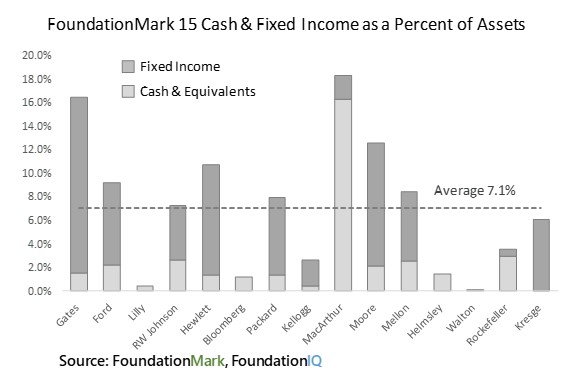

Cash & Equivalents and Fixed Income Allocations

Surprising to readers may be the low levels of cash and bonds revealed by the big foundations’ balance sheets. A possible factor influencing this calculation is that the balance sheet is only reported once a year when the foundation closes its books for the fiscal year. As foundations must distribute 5% of their assets each year, their holdings likely exhibit some seasonality. That said, however, data shows that most foundations in the FoundationMark 15 keep less than 10% of their total assets in cash and bonds, or, stated alternatively, about 90% of their holdings is invested in equities or other investments.

If the Big Ones Vary This Much, Imagine the Smaller Ones ….

One thing that we have learned from following foundations’ assets is that foundations exhibit a wide variety of approaches in investment strategy. Asset allocation can range from cash to cryptocurrency, from a single stock to all in hedge funds, or can incorporate all manner of portfolio strategies in between these. We follow these for a simple reason: We want to see which ones are doing well and then see if other foundations can learn from their success.