News and Analysis of Foundation Investment Performance

How Are Foundations Doing? July 2019 Topic: Is Bigger Really Better?

By

Once a month, FoundationAdvocate selects one topic in foundation-investment performance to highlight.

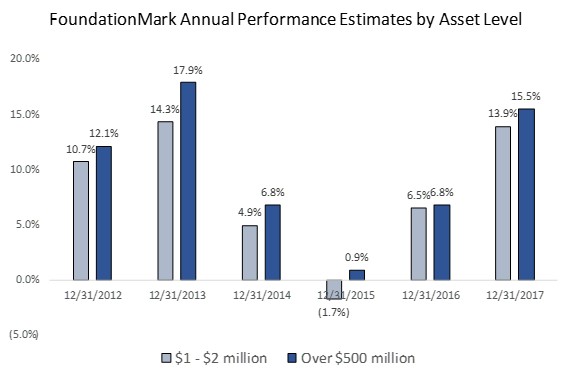

This month’s topic is the relationship between a foundation’s total assets and its performance. The chart below shows the performance of two subsets of foundations, those with assets between $1-$2 million and those with over $500 million.

As you can see from the annualized performance data above, foundations with asset size in excess of $500 million consistently out-performed smaller ones by about 2% per year over the time period shown. We chose to highlight the groups with the largest asset sizes assets (more than $500 million) and the smallest asset sizes that we cover ($1-$2 million) to demonstrate the significance of the performance gap. However, the other levels exhibit a similar pattern, with performance level improving as asset level grows.

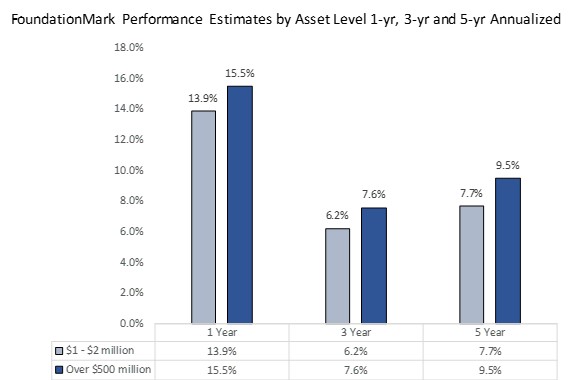

Annualized performance estimates over 1, 3, and 5 years show the consistent trend of out performance by about 2%.

So Larger Foundations Must Be Better Investors, Right?

The natural conclusion that one might draw is that larger foundations tend to be better investors, one explanation of the performance differences. However, two simple factors could also account for much of the performance gap—higher exposure to risk assets and lower investment expenses.

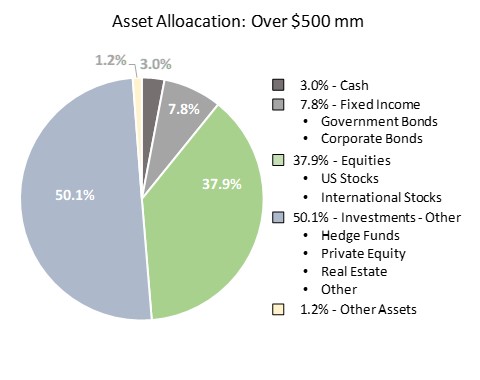

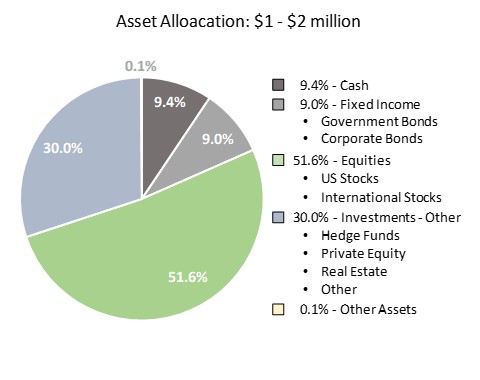

Asset Allocations: Bigger vs. Smaller

As the charts above show, larger foundations had just 10.8% of their assets on average in the lower return/lower risk Cash and Fixed Income categories compared to 18.4% for smaller foundations. In other words, 89% of larger foundations were invested in assets classified as Equities and Investments – Other, the category that includes hedge funds and private equity. With smaller foundations, that number was closer to 82%. After accounting for non-investment assets, the difference was 6.4%.

While a 6.4% difference might not seem like much, consider that, with the S&P 500 up 15.8% per year for the 5-yr period ending December 31, 2017, an incremental 6.4% allocation to the S&P 500 would have boosted performance by 1% per year on average, or more than half the 1.8% difference in the 5-yr returns.

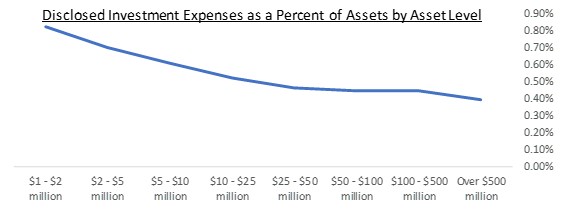

Disclosed Investment Fees

Unsurprisingly, larger foundations have a whole lot more bargaining clout in negotiating investment fees, and many investment products have fee break points for larger accounts.

On average, smaller foundations paid close to 90 basis points in disclosed investment expenses whereas large foundations paid about 40 basis points to cover these expenses, a difference of 50 basis points. (A basis point is 1/100th of 1 percent, and so, for every $1 million in assets, small foundations paid about $9,000 in expenses while large foundations paid just $4,000 per $1 million in assets.) This difference of 50 basis points comprises a little less than one-third of the 5-year out-performance of the smallest foundations by the largest ones.

Not Much Difference After All

Added together, the effects of the large foundations’ more aggressive asset allocation and ability to obtain relatively lower investment fees comprise 1.5% of the 1.8% difference between the large and small foundations’ 5-year performance estimates.

One could argue that the large foundations are better investors as they were right to allocate a greater proportion of assets to higher risk/higher return asset classes over the period. However, one could also argue that larger foundations simply have a greater tolerance for risk. and that doing so makes them better at asset allocation.

That being said, even if large foundations do tend to be better investors, after adjusting for risk levels and fees, the race is probably a lot closer than most people would have thought.