News and Analysis of Foundation Investment Performance

Benchmark Limbo. How Low Can You Go?

By

Custom Benchmarks

In a previous article, Who Controls The Money?, we explored the case that a large part of investment performance is controlled by creating and implementing an investment policy statement (IPS). One factor we highlighted is the use of custom benchmarks. Custom benchmarks are largely the result of the increase in alternative assets. In effect the argument goes, “if we are going to have 10-20% in hedge funds, then the benchmark should have somewhere between 10-20% of hedge fund performance”. The argument is rational.

Marching Orders

Imagine the process at a larger/more institutionalized foundation that has a formal approach to investing – the structure might include the components in the “Institutional Blueprint” below and follow an “Institutional Process”.

Institutional Blueprint

Trustees

Investment Committee

Investment Policy Statement (IPS)

Asset Classes

Asset Ranges

Consultant / CIO / OCIO

Implementation

Asset Allocation

Manager/Security Selection

Institutional Process

The foundation’s trustees might create a subset to serve on the investment committee.

The investment committee, perhaps in conjunction with a consultant, or Chief Investment Officer (CIO) or Outsourced CIO (OCIO) might write an investment policy statement (IPS) laying out the goals and often asset class thresholds. The IPS are typically in place for long periods – 10 years or more.

The foundation may use in-house resources (their own investment staff, which is only the case at the very largest) or hire a firm to implement their policies.

In-house or external money managers invest the foundation’s assets according to the IPS.

The Investment Policy Statement

The investment policy statement (IPS) is a set of guidelines that lay out the general objectives and rules concerning the management of the portfolio. They typically define the types of investments that can be made and offer some structure to the portfolio by creating asset allocation ranges and defining benchmarks. A simple example of the asset allocation might look like this:

Asset Class

Range

Benchmark

Cash

0 – 10%

3 month Treasury

Fixed Income

20 – 40%

Barclays Aggregate

U.S. Equities

30 – 60%

S & P 500

International Equities

10 – 30%

MSCI

Hedge Funds

0 – 10%

HFR Composite

Investment policy statements can be as simple or as complicated as you want as you add in constraints on other factors like volatility, liquidity, concentration, and others. But even in the simple version outlined above, one can begin to see that a lot of the decision making choices for the portfolio has already been narrowed down.

With asset allocation ranges set, and the underlying benchmarks identified, the next step it to define a composite benchmark, typically comprised of the asset class benchmark components, for example 5% 3 month treasury bill, 30% Barclays Aggregate, 45% S&P 500, 15% MSCI and 5% HFR Composite from the example above.

Often Smart, Rarely Brave

If a money manager exceeds the asset allocation ranges, he is liable to get fired, especially if his bet was wrong, so he is likely to stay in the lanes drawn up in the IPS. Furthermore, matching the performance of the composite benchmark is as easy as could be by simply matching the weights of the benchmark. With the ranges and benchmark weights decided, the portfolio manager tries to optimize performance based on the constraints laid out in the IPS. So the manager will use the levers in his control to try to beat the benchmark, for example if he thinks U.S, stocks will do better than international, he will increase the portfolio’s allocation to the U.S. and away from foreign markets. Or if he is worried about stock prices falling, he will load up on cash and bonds.

While it may seem that portfolio managers have significant leeway to change allocation, they tend to “hug” the benchmark allocations, as significant deviation from the benchmark allocation could mean significant deviation in performance. Most institutional portfolio managers are paid according to how much money they run, not how well they perform, so they do not want to run the risk of substantial underperformance (and possibly getting fire), so the easiest way to mitigate the risk of substantial underperformance is to stay close, or “hug” the benchmark,

Adding Complexity

As asset classes have expanded from just stocks and bonds to alternative strategies, like private equity, venture capital, distressed debt, real estate, and commodities, the asset allocation ranges and composite benchmarks have grown increasingly complex. The core (and valid argument) that portfolio managers make is that they want to know how they are going to be evaluated and thus paid. So if, for example the asset allocation range calls for 10-20% in venture capital, there should be an appropriate weighting in the composite benchmark. Naturally different institution may choose different asset classes and different allocation ranges, resulting in many specific benchmarks making comparisons to other institutions difficult. Did the portfolio manager do a good job, or was it just the fact that one institution had a different IPS from the other?

Tall for a Jockey

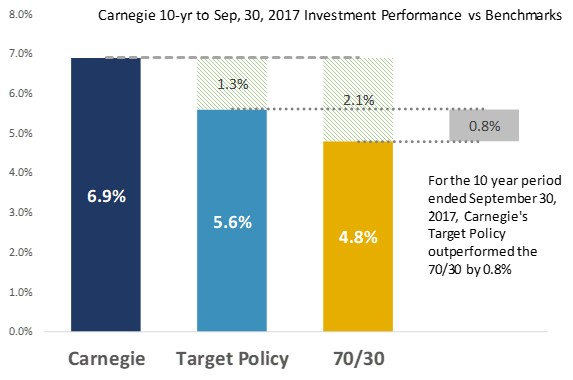

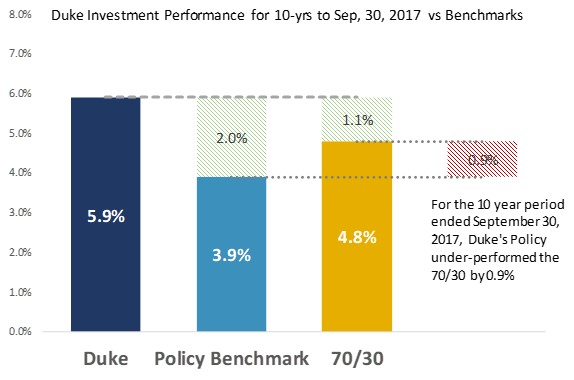

One thing that has puzzled us is that every foundation that reports their investment performance (sadly there are only a handful that do) seems to beat their ‘target’ or ‘policy’ benchmark, much like the children from Lake Woebegone who are all above average.

For example the James B Duke Endowment (not to be confused with Duke University) noted in 2017 that it’s endowment out-performed its policy benchmark by 2.0% per year for the 10 year period. The Carnegie Corporation of New York also outperformed its target policy by a more modest 1.3% per year over the 10 year period. One might draw the conclusions that Duke’s 2.0% out-performance surpassed Carnegie’s. We don’t think that is necessarily the right conclusion.

There aren’t many foundations that publish their investment performance, and even fewer mention their targets. Two exceptions that serve as beacons of transparency are the Carnegie Corporation of New York and the James B Duke Endowment. One thing that we found interesting was the different approaches that they have taken in choosing benchmarks.

When asked about owning his own golf course, country music legend Willie Nelson said, “the best part is getting to set your own par. See that hole? It’s a par 8. Yesterday I birdied that sucker!”